How to Save Up for Your Dreams

From vacation to retirement, keys to reaching your financial goals

For Desirée Daniels and her husband Deryle, seeing the world has always been a big a part of their relationship. After stoking their wanderlust on trips to Mexico, Ecuador and Europe, their most ambitious adventure came last summer.

They explored street markets in Turkey and beaches and jungles in Thailand. They later found inviting back-alley restaurants in Japan before walking the Great Wall in China.

“Our two month trip abroad seemed like one of the rare opportunities you get in life to turn a dream into reality,” said Daniels, a communications specialist for the Nicholas School for the Environment's Office of Development & Alumni Relations. “If you can do it, then why not?”

How they did it was a feat in itself. They scored cheap airfare and affordable lodging, but saving up for the journey required more than a year of drastic lifestyle changes and fiscal discipline.

Whether saving for a trip of a lifetime or retirement, there are time-tested strategies to keep in mind.

Build a Budget

Daniels, who blogged about this trip and many of her other adventures, has always been a good saver, but when her husband convinced her to sit down and craft a budget, she saw how much more she could do.

“We needed to categorize all of our spending and figure out reasonable amounts for each area,” Daniels said.

As they studied expenses, the couple saw how money flowed through their household, and they made informed decisions about changes. Daniels curtailed a few behaviors – like impulse online purchases, which made a measurable difference.

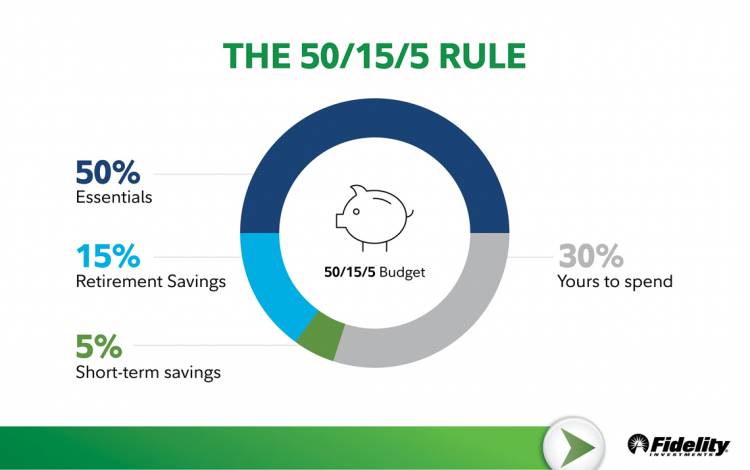

Stay in Balance

Fidelity Investments Financial Advisor Alan Collins recommends the 50-15-5 model while spending and saving.

The idea is that 50 percent of your take-home pay should be allotted for essential expenses such as mortgage, utilities, child care, groceries and paying debt. Fifteen percent of pre-tax income (including employer contributions) should go toward retirement savings and five percent for emergency or short-term savings.

The remaining 30 percent is where you can be flexible and set aside money for whatever you want, or wherever you’d like to go.

“Different things work for different people, but this is a good framework,” Collins said. “If you can do this, you should be OK.”

Think Big Picture

To make their trip happen, Daniels and her husband made painful cuts, trading their spacious apartment for a cramped single-bedroom place, eliminating nearly all restaurant meals and getting by with one car.

To stay on target, they kept the trip front-and-center, discussing it often and spending time researching and making travel arrangements together.

“We had to remind ourselves that in a few months, we’ll do something epic, so the sacrifices made now will only benefit us in the long-run,” Daniels said.

Have a story idea or news to share? Share it with Working@Duke.